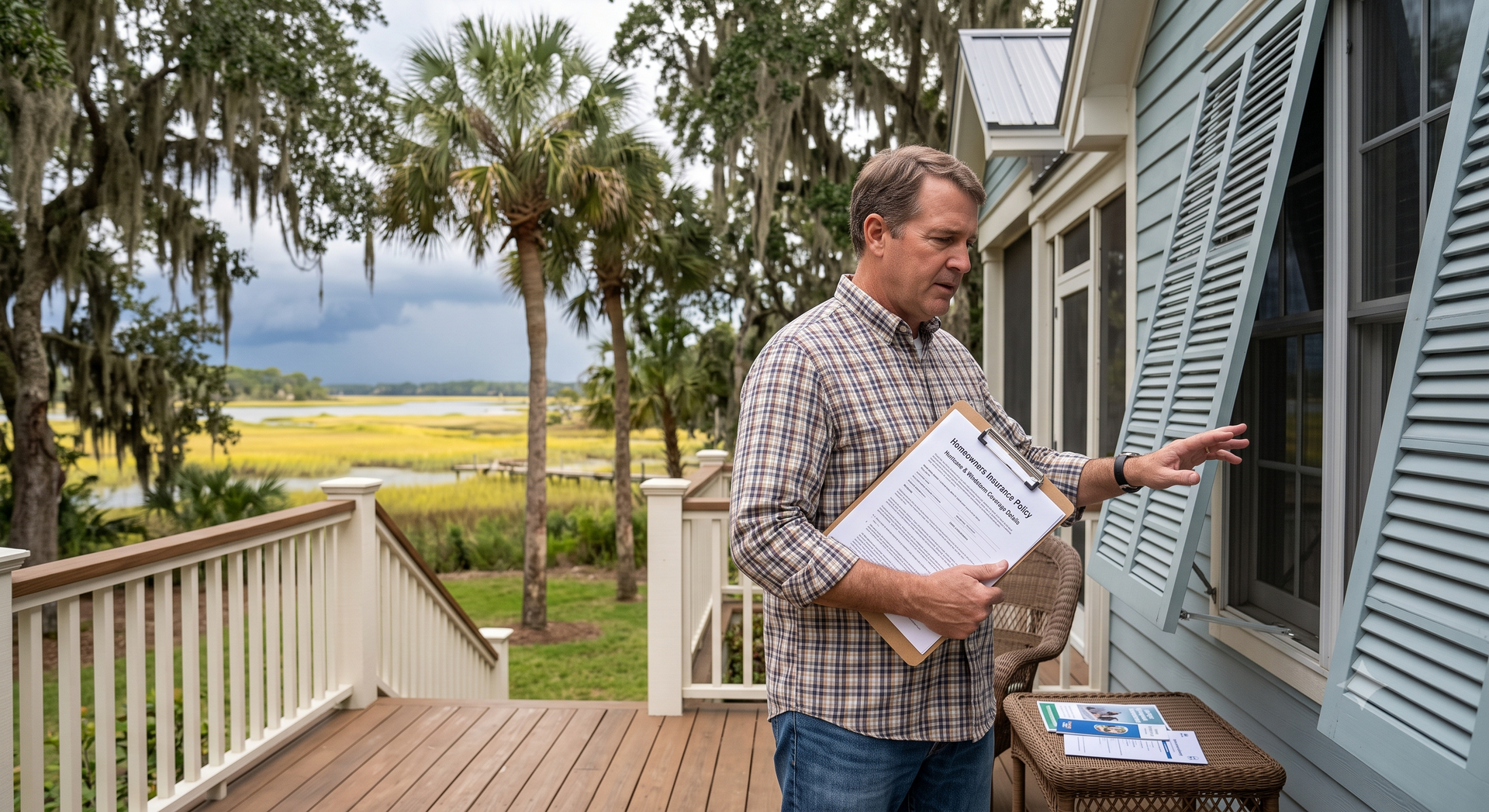

There is no single insurance product called hurricane insurance in South Carolina. What most homeowners mean when they ask about hurricane coverage is really a combination of two separate policies: homeowners insurance for wind damage and a flood insurance policy for storm surge and rising water. Understanding which policy covers which type of damage is one of the most important things a coastal South Carolina homeowner can know. This guide explains how hurricane damage is covered in South Carolina, what each policy handles, where the gaps are, and how to prepare your coverage before storm season arrives. Does homeowners insurance cover hurricanes in SC Standard homeowners insurance policies in South Carolina cover wind damage, which includes hurricane wind. If a hurricane or tropical storm tears off your roof, blows in windows, or damages your siding with windborne debris, your homeowners policy is what responds to those losses. This wind coverage is part of the dwelling protection in a standard policy. However, two important features affect how wind coverage works in coastal South Carolina: Named storm or wind deductibles. Most policies in South Carolina's coastal counties apply a separate, higher deductible to hurricane-related losses rather than your standard flat-dollar deductible. This deductible is typically expressed as a percentage of your dwelling coverage, often 1% to 5%. On a $400,000 home with a 2% hurricane deductible, you'd pay the first $8,000 of any named-storm wind claim before insurance contributes. South Carolina law requires insurers to clearly disclose when a policy excludes wind or applies a special deductible. Availability in coastal areas. Some standard market carriers have restricted or stopped writing new policies in coastal South Carolina due to hurricane exposure. Properties that can't get wind coverage in the standard market can turn to the South Carolina Wind and Hail Underwriting Association (SCWHUA), the state's Beach Plan, for wind and hail coverage as a last resort. Understanding wind and hail exclusions When a standard carrier declines to cover wind and hail for a coastal property, they issue what's called a homeowners policy with a wind exclusion. The home is still insured for fire, theft, liability, and other perils, but anything caused by wind is excluded. The homeowner then needs a separate SCWHUA policy for wind and hail coverage. This two-policy arrangement is common in Myrtle Beach, Pawleys Island, and other beachfront communities. It protects the homeowner against hurricane wind, but it creates additional complexity: two policies to manage, two potential claims processes after a storm, and sometimes ambiguity about which policy covers which damage when a hurricane causes both wind and water damage simultaneously. The SC Wind and Hail Pool (SCWHUA) The SCWHUA is a state-backed program that provides wind and hail coverage to coastal properties that can't obtain it in the standard market. It's the insurer of last resort, not the first choice, and policies through the Beach Plan are typically more expensive than equivalent standard market coverage when it's available. SCWHUA coverage limits and terms differ from standard homeowners policies. Working with a local agent who understands the Beach Plan's current terms and can confirm whether your property qualifies for standard market coverage or requires the Beach Plan is important before binding any coastal property. Storm surge and flooding: why you need separate coverage This is the coverage gap that surprises most people after a major storm. When a hurricane makes landfall, wind isn't the only threat. Storm surge, the wall of ocean water pushed ashore by the storm, is historically responsible for more deaths and property damage than any other hurricane hazard. Inland flooding from rainfall compounds the damage. Standard homeowners insurance, including the wind coverage in a standard policy or a Beach Plan policy, does not cover storm surge or flooding. Water that enters your home from rising water, storm surge, or overflowing waterways is a flood event, and it requires a separate flood insurance policy to be covered. The National Flood Insurance Program (NFIP) provides the standard flood coverage option for South Carolina homeowners. Private flood insurers offer an alternative with sometimes better pricing or higher limits. The NFIP caps building coverage at $250,000, which may be insufficient for higher-value coastal homes. Both NFIP and private flood policies require purchase well before a storm, typically with a 30-day waiting period for NFIP coverage. Buying flood insurance after a storm is named or forecast provides no protection from that event. How much does hurricane insurance cost in SC The combined cost of homeowners insurance with wind coverage and flood insurance varies significantly based on your property's location, its distance from the coast, your home's construction and elevation, and which carriers you use. For a Myrtle Beach homeowner with a standard policy covering wind, average homeowners insurance premiums run $2,678 to $3,100 per year for $300,000 in dwelling coverage at the state average. Coastal and beachfront properties pay considerably more. The average NFIP flood policy in Myrtle Beach runs about $386 per year. Properties in high-risk AE or VE flood zones pay more, often $1,000 to $3,000 or more annually, depending on elevation, construction type, and coverage amount. Together, a well-structured coverage package for a coastal South Carolina home typically includes homeowners insurance with wind coverage, plus a flood insurance policy. For properties requiring the Beach Plan for wind, add the cost of two separate policies. Preparing your home for storm season Coverage decisions matter most before a storm arrives. After a named storm is forecast for South Carolina, purchasing new policies or making significant coverage changes may not take effect in time. A few things worth doing before hurricane season each year: Review your homeowners policy's hurricane deductible and confirm the percentage that applies to your dwelling coverage value. Confirm whether your policy covers wind or has a wind exclusion, and if excluded, verify your SCWHUA coverage is current. Ensure your flood insurance is active. If you don't have it, initiate the 30-day waiting period now rather than in August. Check your dwelling coverage limit against current rebuild costs. Construction costs have risen significantly since 2020, and an outdated coverage limit can leave you underinsured after a total loss. Document your home and its contents with photos or video. Store that documentation in the cloud or off-site so it's accessible after a storm. Getting coastal coverage right Coastal South Carolina insurance requires local knowledge. Which carriers currently write in your specific ZIP code, whether the Beach Plan applies to your property, and how to structure wind and flood coverage together all depend on your home's specific situation. Moore & Associates has served the Grand Strand since 1979 and helps homeowners navigate these decisions every day. Our homeowners insurance team compares coverage from multiple carriers and explains exactly what each policy covers and doesn't. Call (843) 839-5076 or visit mooremb.com for a free consultation. We serve Myrtle Beach, North Myrtle Beach, Surfside Beach, Murrells Inlet, Litchfield, Pawleys Island, Conway, and Georgetown.

Flood insurance in South Carolina is not included in any standard homeowners or renters policy. If your home or its contents are damaged by rising water, storm surge, or a flooded waterway and you don't have a separate flood policy, you pay for that damage out of pocket. For most South Carolina homeowners, particularly those on the coast or near rivers, lakes, and tidal areas, the question isn't really whether to get flood insurance. It's how much it costs and where to buy it. This guide covers both. Average flood insurance costs in South Carolina The average NFIP flood insurance policy in South Carolina currently costs around $929 per year according to FloodPrice's 2025 analysis, though costs vary significantly by location and coverage amount. Statewide averages in other analyses range from $672 to $798 depending on the data set and the mix of high-risk versus low-risk properties included. In Horry County, which includes Myrtle Beach, the average NFIP premium is around $448 per year across approximately 22,000 active policies. Myrtle Beach itself averages about $386 per year. North Myrtle Beach runs higher at approximately $476 per year. Surfside Beach, which has a higher concentration of beachfront properties, averages around $647 per year. These averages reflect the current NFIP pricing under Risk Rating 2.0, FEMA's updated methodology that prices each property individually rather than based solely on flood zone maps. The new system considers a property's flood frequency, the type of flooding it faces (coastal surge, river overflow, heavy rain), its distance from water, its elevation, and the cost to rebuild. FEMA estimates that 66% of policyholders nationally will see premium increases under this system as rates move toward full actuarial risk levels. NFIP vs private flood insurance pricing The National Flood Insurance Program (NFIP), managed by FEMA, is the primary source of flood coverage for most South Carolina homeowners. NFIP policies are available to any property in a participating community, which includes Horry County and all municipalities along the Grand Strand. The NFIP caps building coverage at $250,000 and contents coverage at $100,000. Private flood insurance is an alternative that can provide higher coverage limits, shorter waiting periods, and sometimes lower premiums than the NFIP for the same property. Private policies can serve as standalone coverage or as excess coverage above NFIP limits for higher-value properties. Comparing both NFIP and private quotes is worth doing before purchasing, particularly for properties with rebuilding values above $250,000. The NFIP's standard 30-day waiting period applies to most new policies. If you purchase an NFIP policy today, it doesn't take effect for 30 days. Private flood policies often have shorter waiting periods, sometimes as little as 10 to 14 days, which matters for homeowners purchasing before storm season. The 30-day waiting period has exceptions for new home purchases where flood insurance is required by a lender. Flood zones in Horry County FEMA flood zone designations affect both your flood risk and your insurance costs. The main zones relevant to Horry County and the Grand Strand are: Zone AE : High-risk Special Flood Hazard Areas with established base flood elevations. Properties with federally backed mortgages in Zone AE are required to carry flood insurance. Annual flood probability is 1% or higher. Zone VE : Coastal high-hazard areas subject to wave action as well as flooding. The most expensive zone for flood insurance and the highest-risk designation for beachfront and near-beach properties. Zone X : Moderate to minimal risk areas. Flood insurance is not required by lenders here, but flooding still occurs. About 25% of all NFIP flood claims nationally come from properties in X zones. FEMA's flood maps don't always reflect current risk accurately, particularly given how conditions have changed since many maps were last updated. For a more current view of your property's flood risk, FEMA's Risk Factor tool provides a property-specific assessment that accounts for current data. Factors that determine your flood insurance premium Under Risk Rating 2.0, the NFIP calculates premiums based on several property-specific factors: Your property's distance from the nearest water source, whether ocean, river, canal, or tidal creek. The flood frequency your property faces based on historical and modeled data. The type of flooding risk, coastal surge, interior flooding, or heavy rainfall runoff. Your property's elevation relative to the base flood elevation for your area. The replacement cost of your structure, since higher-value homes cost more to insure. The foundation type, slab, crawlspace, elevated, or basement. Properties built elevated above the base flood elevation, particularly on pilings or posts in coastal areas, typically pay lower flood premiums than equivalent homes built at or below flood level. Elevation certificates, which document your home's elevation relative to the local base flood elevation, can help confirm your premium accurately reflects your actual risk. Ways to reduce your flood insurance cost Several strategies can reduce what you pay for flood coverage in South Carolina. Elevate the property or utilities. Raising your home or moving electrical panels, HVAC equipment, and other utilities above the base flood elevation directly reduces risk and typically lowers premiums. Choose a higher deductible. NFIP policies allow deductible choices that affect premiums. Higher deductibles reduce annual cost but increase out-of-pocket exposure on a claim. Check your community's CRS rating. The Community Rating System (CRS) gives communities discounts on NFIP premiums when the local government implements floodplain management practices above the minimum NFIP requirements. Some South Carolina communities have CRS ratings that qualify their residents for discounts of 5% to 45%. Compare private market options. For some properties, private flood carriers offer lower premiums than the NFIP for similar coverage. Getting both quotes is worth the time. Don't wait until storm season The 30-day NFIP waiting period makes timing critical for coastal South Carolina homeowners. Purchasing flood insurance when a storm is approaching gives you no protection from that event. Moore & Associates helps clients evaluate both NFIP and private flood options and navigate the coverage decisions specific to coastal South Carolina properties. Visit our flood insurance page or call (843) 839-5076 for a free consultation. We serve Myrtle Beach, North Myrtle Beach, Surfside Beach, Murrells Inlet, Pawleys Island, Conway, and Georgetown.

General liability insurance in South Carolina: what it covers, what it costs, which businesses need it, and how to choose the right coverage level for your operations.

Own a Jet Ski or Sea-Doo on the SC coast? Learn what personal watercraft insurance covers, what it costs, and why Grand Strand riders need it. Get a free quote.

South Carolina car insurance laws require 25/50/25 liability plus mandatory UM coverage. Here's what the minimums mean, why they're often not enough, and what else to carry.

Best homeowners insurance companies in South Carolina for 2026: Chubb, Allstate, State Farm, USAA. Average costs, coastal considerations, and what to look for.

Myrtle Beach home insurance in 2026 costs more than it did five years ago and covers differently than policies in most of the country. Here is what every Grand Strand homeowner needs to understand about wind, flood, costs, and coverage gaps.

Auto insurance in Myrtle Beach is shaped by SC's coverage requirements, coastal weather, and some of the highest tourist traffic volumes on the East Coast. Here is what you need, what it costs in 2026, and how to save.

Learn what mobile home insurance covers in South Carolina, how much it costs near the Grand Strand, and how to avoid common coverage gaps. Get a quote today.

SC renters insurance costs $12 to $20 a month and covers your belongings, liability, and temporary living expenses if your unit becomes uninhabitable. Here is what you need to know before buying a policy in South Carolina.