Learn how HOA insurance in South Carolina works, what the master policy covers, and where your personal coverage must fill the gaps along the Grand Strand

Find out how much car insurance costs in South Carolina. Local Grand Strand rates, required minimums, and tips to lower your premium from a Myrtle Beach agent.

Shopping for car insurance in Georgetown, SC? Learn SC minimums, local flood and storm risks, and how an independent agent finds you the best rate. Get a free

Learn South Carolina's auto insurance minimums, what 25/50/25 really covers, and why Grand Strand drivers often need more. Get a free quote from Moore &

Protect your Conway home from flood damage. Moore & Associates compares NFIP and private flood insurance options in Horry County. Get a free quote today.

Get homeowners insurance in Surfside Beach, SC from a local independent agent. Moore & Associates specializes in coastal coverage. Free quote today.

What does renters insurance cover in SC and how much does it cost? Get the facts from a local independent agent. Free quotes from Moore & Associates.

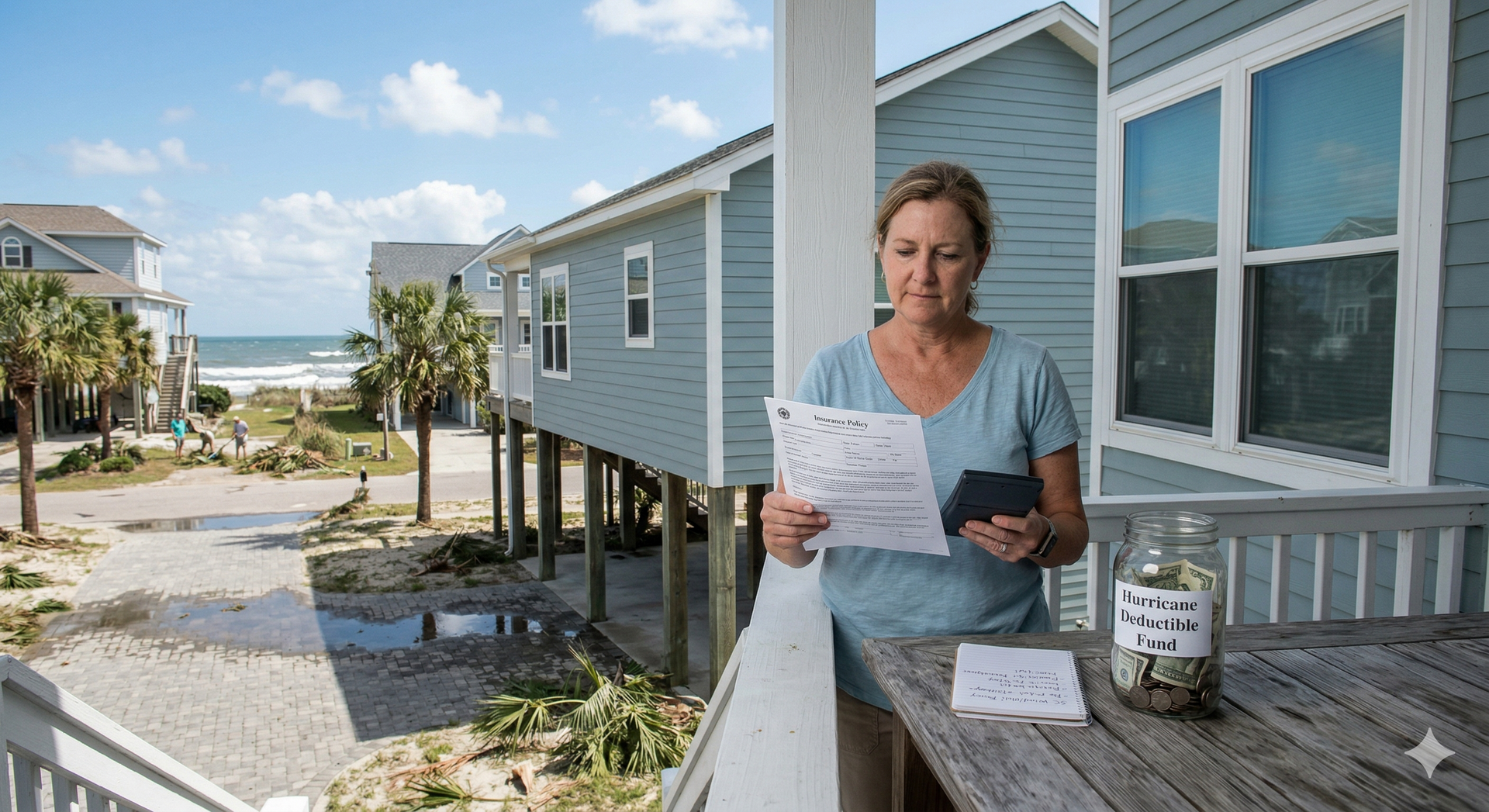

SC hurricane deductibles work differently than standard deductibles. Learn what coastal homeowners must know before hurricane season. Free quote available.

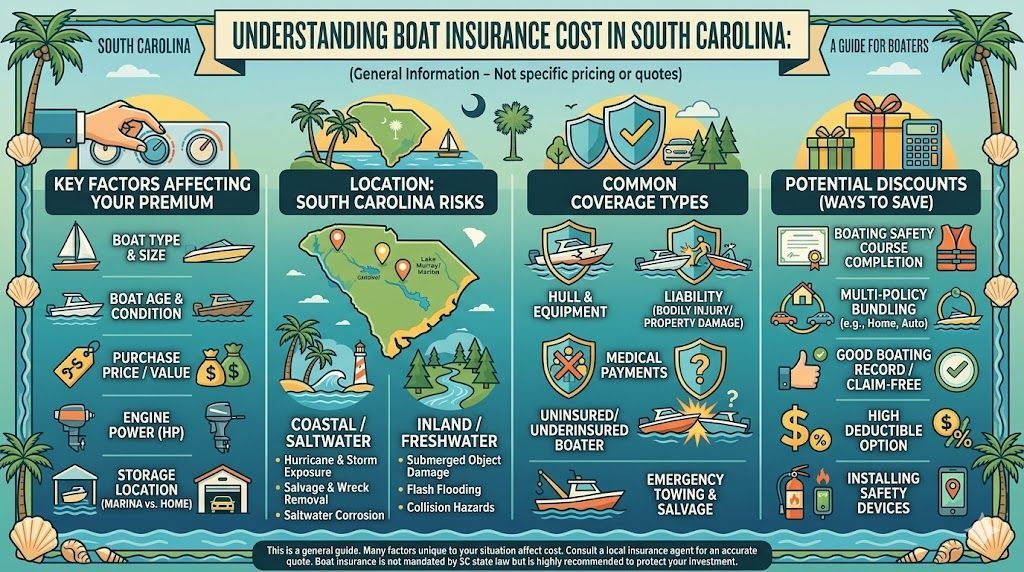

How much does boat insurance cost in SC? Learn what factors affect your rate and how to get the best coverage. Free quotes from a local Myrtle Beach agent.

Get homeowners insurance in North Myrtle Beach, SC from a local independent agent. Moore & Associates compares coastal coverage from top carriers. Free quote.